If you occasionally or even frequently experience negative cash flow, you’re not alone. Even brands that are household names, like Tesla, experience cash flow problems from time to time.

Across all industries, business owners struggle to keep a steady flow of incoming cash for the business in order to meet their payroll, inventory, and other operating expenses and financial obligations.

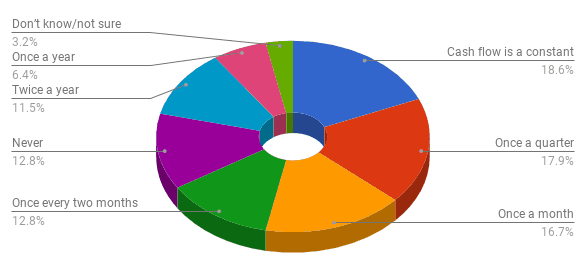

The cash flow crunch affects some types of companies more than others. In the construction industry, for example, a recent Tsheets by Quickbooks survey found that 87% of construction companies experience cash flow problems. Of those, 47.4% experience negative cash flow monthly to quarterly. For 18.6% of these companies, healthy cash flow is a constant problem.

How often does your [construction] business experience a cash flow problem?

Source: Tsheets (Quickbooks)

Even Big Brands Experience Negative Cash Flow

If you’re beating yourself up over your cash flow woes, stop! It’s a common misconception that gaps in cash flow are caused by poor financial management or a lack of business planning. Even massive brands like Tesla run into trouble. In fact, these major companies have all experienced cash flow issues over the past few years:

- General Electric was forced to sell off parts of its business, as mounting debt and reduced operational revenue contributed to a cash flow crisis.

- Netflix reported nearly negative cash flow of $560 million in Q2 2018 as it poured funds into new content creation, amidst questions about its content accounting practices.

- General Motors (GM) sat at about -$12 million free cash flow for a solid year. Volvo and Jaguar Land Rover were also operating with negative free cash flow throughout 2018, as well.

- African phone giant MTN may also experienced a cash flow crunch after being ordered to pay $10 billion in taxes and dividends the government says it should not have taken home.

So you see, if you’re having cash inflow issues despite running a business that’s profitable based on operational or investment revenue, you’re not alone. In fact, you’re in some pretty great company.

Of course, it’s not necessarily the company you want to keep. Developing a proactive strategy to prevent gaps in cash flow will keep you out of crisis in the first place. If you’re not sure where to start when it comes to managing your cash flow, our Ultimate Cash Flow Guide walks you through the must-dos and must-knows, step by step.

This article looks at some of the financing options that your business can use to either mitigate negative cash flow or use if it’s currently experiencing poor cash flow.