Get an overview and comparison of small business lending options so you can make the best choice for your business.

It can be challenging to get funding for small- and medium-sized businesses, whether you’re a new business in the startup stage or an established business in the growth stage. It’s something we understand first-hand as entrepreneurs ourselves here at FundThrough. We know what it’s like to need working capital for payroll or growth, and not know what your options are. Securing bank financing can leave you feel like you’re jumping through hoops, what with the lengthy application processes and all that paperwork. On top of that, traditional bank financing requires your business to have a solid financial track record and good credit, something many new and growing businesses might not have. Banks often don’t want to work with new businesses, and even growing businesses can get denied a limit raise on their business line of credit. The solution to these challenges for many businesses is to create a mix of funding sources from options outside the traditional banking system, like equity financing and alternative funding methods. If that’s you, read on to get an overview of several small business lending options along with their pros and cons so you can make the best small business lending decisions for your company.

Consider these aspects of your situation when evaluating financing options. This list isn’t exhaustive, but will give you an idea of what to take into account and help you get the best value from your business financing options:

Invoice factoring is a type of small business lending. Since invoice factoring is not a loan, it doesn’t require you to give up equity in your business or take on any debt in order to secure funding. (See more alternatives for non-dilutive funding.) How it works is that a business sells outstanding invoices to a factoring company for access to business capital. The factoring company then works with your customer to settle the invoice according to the original payment terms. You get access to funds in a few business days, while the factor manages the collections process on your behalf. Many of our clients factor invoices when they need cash upfront for a big growth opportunity, cover business expenses, or even peace of mind about making payroll.

Pros:

Cons:

Bridge financing loans can be a useful option for businesses looking to fund short-term needs. It can help you cover expenses until more traditional long-term funding can be secured. You might also use bridge financing to speed up the payment cycle instead of waiting on lengthy net terms. A bridge financing loan helps to literally bridge the gap between rounds of investor funding, when loan applications or business lines of credit are denied or delayed, or during an IPO.

Cons:

Consider these bridge capital factoring alternatives if a bridge financing loan is not the right small business lending option.

In a marketplace lending (AKA peer-to-peer lending) platform, the decision-making structure is decentralized. This is in contrast to personal and small business banking, which operate under centralized decision-making structures. Each online lender sets their own lending standards with borrowers directly, and makes their own choices about who to approve within the loan program. As such, the limits of loans can be adjusted as a borrower’s needs change. There are also platforms and online lenders that cater specifically to businesses with bad credit or no credit history.

Pros:

Cons:

Venture capital (VC) is a type of private equity financing that is typically provided by high net worth individuals, institutional investors, or investment banks to start-up or early-stage companies with high growth potential.

Pros:

Cons:

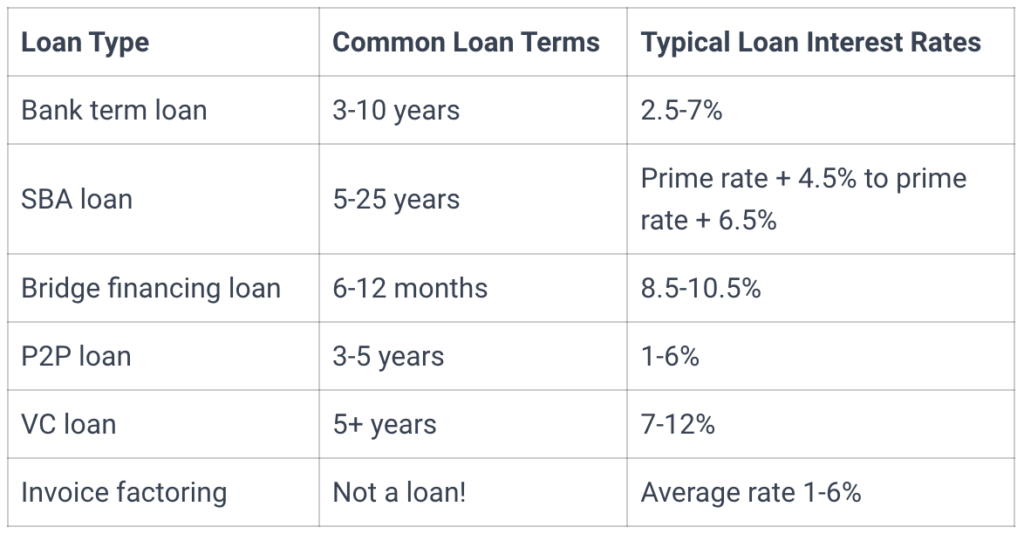

Here’s a brief, high-level explanation of how small business loans work: You research the various business financing options available and find one that meets your business needs. From there, you to submit an application outlining your business plan and financial history in order to be approved for the loan. In our experience, many of our small business clients are denied for various loan types and often have to look for other types of financing and small business lending to meet their needs. If you meet the business loan requirements and your application is approved, you will receive the loan funds and be required to start your repayment term according to the terms of the loan. Depending on the type of loan, you may have a repayment period that could span from months to years, with actual interest rates ranging from single digits to double digits depending on your credit score and other factors. See the table below for more insight on actual interest rates.

The most important step towards getting approved for a small business loan is to ensure that you have a complete and accurate application. Depending on the type of small business lending you’re applying for, you may also need several years worth of financials that show growth, a strong cash position, and a good credit score.

The best kind of loan for a small business is one that meets your unique business needs, has flexible repayment options, the lowest interest rate, dedicated customer service, and is specifically designed for small businesses. Look for ones with favorable repayment terms such as no prepayment penalties or balloon payments.

The minimum credit score for a small business loan can vary greatly depending on the type of lender you work with. While some lenders require excellent credit scores of at least 680+, some business lenders with programs for bad credit will work with borrowers with credit scores that are less than ideal. Invoice factoring doesn’t require a credit check. Your customer’s creditworthiness is more important than your own, since the factoring company depends on them to pay their invoice.

See if you qualify to fund an invoice now.

Speak with your dedicated account manager on the phone or online.

Interested in possibly embedding FundThrough in your platform? Let’s connect!