Increase your cash flow quickly with your own receivables

WHAT'S IN THIS GUIDE

The project-based nature of engineering firms’ work is a challenge that can lead to lumpy cash flow. This is on top of the 30, 60, or 90-day payment terms common within the engineering industry, which prolong the payment cycle even further. This makes it tough to keep up with expenses like labor, other operating costs, and to take on big projects that would help your business grow. We understand the difficulties cash flow challenges like this cause since we’re entrepreneurs ourselves, as well. Engineering invoice finance offers a solution to these cash flow crunches, and helps smooth cash flow so you can more easily manage your expenses and go after business growth opportunities.

Invoice factoring for engineering firms is a financial arrangement that allows an engineering firm to improve its cash flow by selling its accounts receivable, or outstanding invoices, to a factoring company. Invoice factoring provides immediate access to funds that would otherwise be tied up in unpaid invoices, allowing engineering firms to meet their immediate financial obligations and fund their operations more effectively.

Invoice finance for engineering is a financing solution specifically designed for engineering firms to address their cash flow needs. It is similar to invoice factoring, but with some key differences.

In engineering invoice financing, an invoice finance company or lender provides a loan or line of credit to the engineering firm based on the value of its outstanding invoices. Instead of selling the invoices outright as in invoice factoring, the engineering firm uses the invoices as collateral to secure the financing from the invoice finance company. That said, often times invoice financing is simply used as another term for invoice factoring.

The engineering invoice factoring process with FundThrough is actually pretty straightforward. Here’s how it works:

Create a free account or connect your QuickBooks or OpenInvoice account, and provide information about your business.

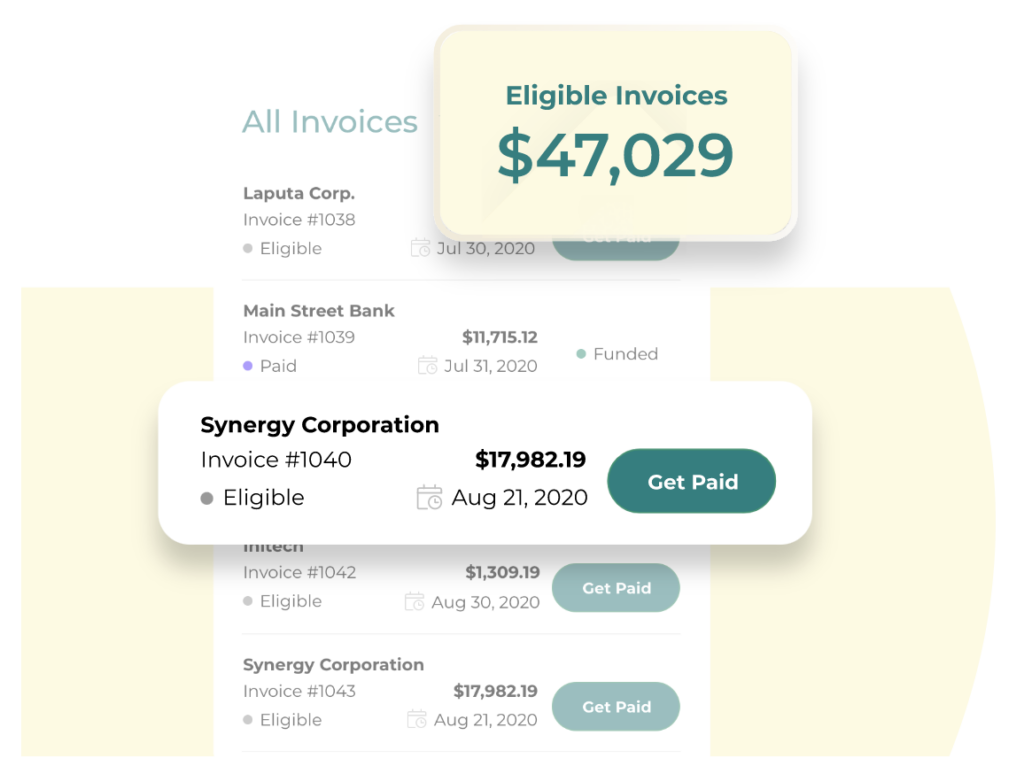

Upload invoices into FundThrough or pull in eligible invoices from QuickBooks or OpenInvoice. We provide unlimited funding for your business based on the size of your outstanding invoices.

Select which invoices you want to fund, and submit them in one click (after set up).

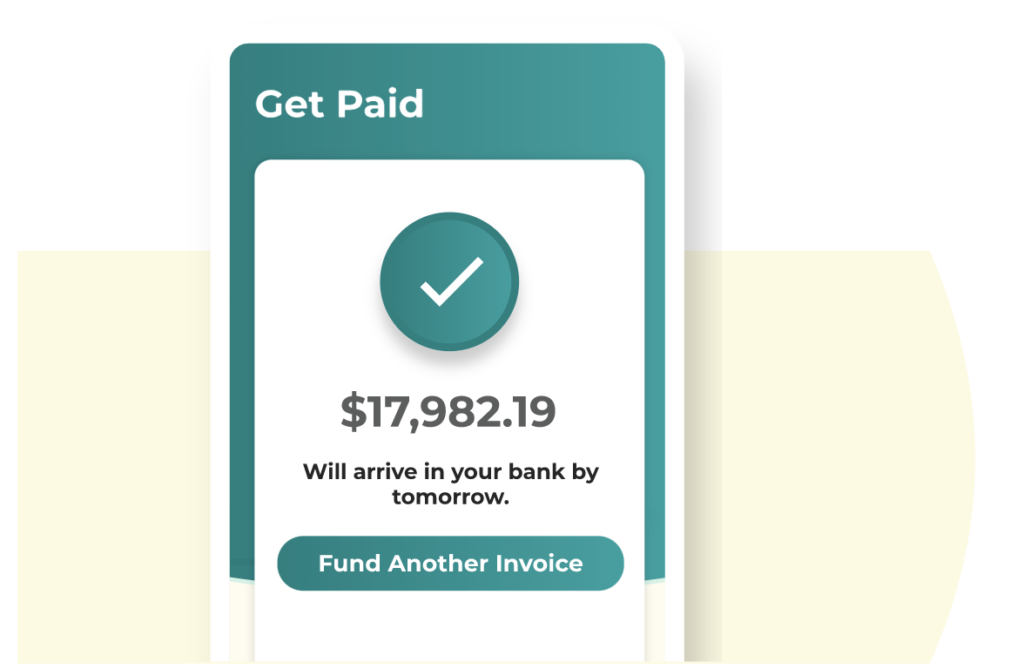

Upon approval, funds are deposited into your business bank account as soon as the next business day.

You can then put your capital to work for growth projects, payroll, equipment, hires, and more.

Factoring gives engineering firms access to the cash they’ve already earned. If you’re considering invoice factoring, here are just some of the benefits of invoice finance for your firm.

Like most business funding options, engineering factoring is not without its drawbacks.

In the past, many factoring companies were aggressive with collecting payment from customers, which led to engineering factoring getting a bad rap. Nowadays, reputable companies work with you before contacting your customer. At FundThrough, we know how hard you’ve worked to build your customer relationships, which is why we treat your customer like our own.

There’s a perception that accounting for factoring transactions in bookkeeping software can be difficult, but once you’ve seen the process broken down step by step, it’s manageable. Our blog post shows you how to record factoring transactions in QuickBooks and other accounting software.

Until invoice factoring became an option to help small, growing businesses get funding, business bank loans, lines of credit, and credit cards were the traditional and accepted forms of financing. Depending on your situation, each of these different funding options can be appropriate. We’ve put together the pros and cons to help you choose the best way to fund your business.

Loans

Costs for a new or growing business can be significant. You may need to purchase equipment and inventory, pay employees, and keep up with rent, taxes, and marketing. You may consider taking out a business loan.

Pros

Cons

A line of credit (LOC) is a lot like a credit card. You can borrow/withdraw money up to a certain maximum amount determined by your financial institution. You can cover day-to-day expenses and pay back your debt, only to borrow again when needed.

Pros

Cons

Like all forms of funding, business credit cards must be used wisely. It can be easy to overspend with a credit card.

Pros

Cons

Invoice factoring pays your outstanding receivables in days, unlocking working capital you’ve already earned.

Pros

Cons

Choosing a factoring partner is a lot like choosing any lender. You’ll have to talk to each finance partner you’re considering to find the right fit for your business. We recommend asking these questions:

Most factoring companies work with most industries, but not all. Some factors specialize in only a few industries.

FundThrough works with engineering companies.

The advance rate refers to the percentage of the invoice value that a factoring company is willing to advance upfront to the business selling the invoice. For example, if the advance rate is 80% and the invoice value is $10,000, the factoring company will provide an instant cash advance of $8,000 to the business and send the rest of the total, less their fee, once the customer pays the invoice. Advance rates can range from 60% to 100%, depending on the factoring company and sometimes the industry.

FundThrough advances 100% of the invoice amount, less a fee.

FundThrough pricing – 100% advance rates minus a flat fee. One up front price.

A minimum is the amount you must factor every period (month, quarter, or year). Some factoring companies offer plans that require minimums, while others do not.

FundThrough doesn’t require minimums. Only fund when you need to.

Cash flow is the number one problem for most start-ups and small businesses, especially if they’re growing. This is also true for engineering firms. Invoice factoring companies typically consider the following before offering you an advance.

Factoring invoices is a sound financial strategy if:

Built For Your Business.

Interested in possibly embedding FundThrough in your platform? Let’s connect!