Ask FundThrough

Invoice Factoring

Invoice Factoring Rates: How to Find the Best Deal for Your Business

By FundThrough

If you’ve ever shopped for any kind of business funding, one of the first questions you’ll have is about the rates. You have to know what you’ll pay to borrow money (or in the case of invoice factoring and invoice financing, having your cash now as opposed to 30 days or more) and evaluate whether you’re getting a fair price and if that price provides enough value. That’s why we’re diving into everything you need to know about invoice factoring rates in this post. You’ll find answers to common questions, enabling you to accurately weigh any offer you get from a factoring company.

What is a typical factoring rate?

Average factoring and invoice financing rates vary somewhere between 1 and 6 percent. The main factoring fee is called the transaction fee or discount rate. This is the amount of money that the factoring company withholds from the invoice total as their payment for advancing cash and waiting to get paid for you. However, interest rate isn’t the only information to consider when you’re evaluating offers from factoring companies.

Evaluating Factoring Offers: 7 Things to Consider

When you’re considering an invoice factoring offer, ensuring you’re getting a fair deal involves more than just the headline numbers. Here are critical aspects to consider:

1. Price and fee transparency: Understanding the full cost of factoring goes beyond the base transaction fee. Many factoring companies layer on additional fees, which can seriously impact the total cost. Be wary of various fees such as adjudication, annual review, monthly maintenance, exception, payment, and passthrough fees. Also, be mindful of late payment penalties and increased interest rates for past-due payments. The key is to get full transparency to avoid any hidden costs that can accumulate over time.

2. Contract flexibility: Unlike many factoring companies that require a 12-month commitment, some, like FundThrough, offer more flexibility with spot factoring. This approach allows businesses to select specific invoices for funding on an as-needed basis, giving you greater control over your cash flow and avoiding unnecessary costs for unneeded services.

3. Minimum volume requirements: Traditional factoring agreements might require you to factor 100% of your invoices, which can be excessive and expensive if you only need a fraction of your receivables advanced. Even if the interest rate seems higher, funding a smaller portion of your A/R with a company like FundThrough could result in lower overall costs, making it a smarter financial decision.

4. Service Level Agreements (SLAs): The efficiency of the factoring service is crucial. Ask about the time frames for funding after invoice submission, especially for passthrough payments. For example, FundThrough offers rapid processing, capable of same-day funding (after first funding with a customer). This speed can be a significant advantage in managing your cash flow effectively.

5. Reputation: The factoring company’s reputation is important since they will be directly interacting with your customers. A reliable factoring partner should treat your clients professionally and ensure a smooth process. There are several credible sources that can help you make a decision when it comes to finding the right funding partner. FundThrough’s strong reputation is evidenced by its partnerships with QuickBooks and Enverus, high customer satisfaction ratings, and recognition as the Best Overall Factoring Company by Forbes Advisor for 2024.

6. Advance Rates: This is the percentage of your invoice that factoring companies initially advance you; when your customer pays the invoice they then send the remaining balance less fees. Advance rates can vary from 80% to 95% of the invoice value, meaning that you’ll wait to get anywhere between 5% to 20% of your funding. If you’re trying to improve your cash flow, you’ll need to ensure that you still have enough funds to cover the gap after the advance rate is applied. This is why FundThrough offers 100% advance rates, less one flat fee.

7. Recourse vs Non-Recourse: With non-recourse factoring agreements, if your client doesn’t pay their invoice, you won’t have to repay the advance–but they’re more expensive than recourse. If your client is creditworthy, you can save money with a recourse factoring agreement.

Ready to fund your invoices for the best deal?

What are factoring fees?

The fees you can expect vary between companies. In addition to the percentage a factor keeps, sometimes there are hidden fees to watch out for:

- ACH fee: This is the fee for the factor’s bank wiring funds to your account, passed on to you. Also known as a wire fee.

- Application fee: A flat or percentage fee that’s highly variable. It can also be called an origination fee.

- Invoice processing fee: A fee charged for getting your unpaid invoices processed in the back office.

- Closing fee:An additional amount the factoring company keeps from the invoice

- Monthly fee: If you sign a contract requiring that you sell a certain portion of your invoices on a monthly basis and you don’t meet the minimum, you could end up paying this fee.

- Termination fee: Again, this applies if you signed a factoring agreement or long-term contract and want to end it early.

- Adjudication fee: Charged for doing a credit check on your customer.

- Annual review fee: An annual charge for the review of your account.

- Exception fee: Incurred for invoices that require additional handling or deviate from normal processing.

- Payment fee: Assessed for processing payments from your customers.

- Passthrough fee: Applied when forwarding non-advanced payments to the client.

- Late payment penalty fee: Charged when payments from customers are late, in addition to the factoring fee.

- Interest rate penalty for past-due payments: An increased rate applied to the outstanding amount when payments are overdue.

It’s easy to see how hidden fees can add up over time, making it important to ask any factoring company you’re considering about their average accounts receivable factoring rates and any additional fees.

To give you our perspective, FundThrough’s current invoice factoring rates depends on your individual circumstances. Our invoice factoring rate is 2.75 percent per 30 days. We don’t charge any hidden fees, and you’re not locked into a contract obligating you to fund invoices; rather, you can choose which invoices to fund when it makes sense for you. Because we believe in transparency, we clearly communicate your total cost of invoice factoring before you fund, so you can make an informed decision. See our pricing page for more on what you can expect to pay for invoice funding.

Ready to fund your invoices for the best deal?

What determines invoice factoring rates?

Invoice factoring rates depend on the company and how they charge for advancing your invoice. Some of the factors that can influence the final price include:

- The invoice terms: Shorter terms, like Net 30, usually come with lower rates compared to longer terms such as Net 60, assuming timely payment by your customer.

- Size of the invoice: Bigger invoices might attract lower factoring fees, as some companies reduce rates for larger amounts.

- Who your customer is: The better your customer’s credit, the lower the risk for the factoring company, which can lead to better rates for you. (Bad credit results in rejection.)

- Industry: Factoring rates can vary by industry, especially if your sector is considered high-risk. Finding a factor that specializes in your industry, like oil and gas or other specialized fields that use factoring are options.

- Volume of invoices: Consistently factoring a large volume of invoices could qualify you for lower rates, as it represents steady business for the factoring company.

- Recourse vs non-recourse factoring: In recourse factoring, you’re responsible if your customer fails to pay the invoice. Non-recourse factoring removes this risk from you, but usually at a higher cost due to the factoring company taking on more risk.

Factoring Fee Types

There are several ways invoice factoring companies charge for their factoring services, including flat rate, variable rate, and prime plus margin fee (a type of variable pricing). We’ll explore them below, so you have a better understanding of common factoring rate structures, and how to get the best invoice factoring rates for your needs.

The difference between flat rate vs tiered rates (aka variable invoice factoring rates)

A flat factoring rate, or flat fee, is exactly what it sounds like. The factoring company charges a flat percentage for every invoice. After you’ve paid that price up front, you don’t pay anymore for as long as the invoice stays open.

Tiered factoring rates, also known as variable invoice factoring rates, are more complicated. Typically the factor will take a percentage of the invoice for as long as it goes unpaid. The upside is that if your customer pays promptly, you might save money with a variable rate. Here’s an example based on our own pricing, which is 2.75% per 30 days. The cost of factoring is deducted from your advance and is based on when the invoice will be paid:

1-30 days = 2.75% • 31-45 days = 3.75%

46-60 days = 5.5% • 61 days and up = 8.25%

Prime plus margin invoice factoring rates

Another model you’ll find sometimes is prime plus margin fee. In this style of pricing, the factor uses the prime interest rate (whatever it is that day) and they charge you a percentage on top of that. So if the prime rate is 3.25 percent + 2 percent discount rate, you’d be charged an invoice factoring rate of 5.25 percent. Unless the prime rate only applies to your advance rate. Some factors only advance a certain portion of the invoice, say 80 percent, and will only forward the rest when the invoice (less the discount rate) is paid.

Master Your Cash Flow

Everything you need to master cash flow basics in a comprehensive guide and template.

Invoice Factoring Rate Examples: Flat vs Tiered vs Prime Plus Margin

Let’s go over an example of factoring an invoice using the different ways factoring companies structure their factoring fees to give you an idea of what to expect with different fee structures.

Flat rate factoring fee example

Say you factor a $100,000 invoice that’s due in 60 days. The factoring company charges you a flat rate of 5% in order to factor your invoice. This means that you get an advance for $95,000, and pay a $5,000 invoice factoring fee. With flat rate factoring, you would be charged the same amount (in this case, 5%) even if the invoice due date was 30 days or 90 days, or, if the invoice was twice as big.

Tiered factoring fee example

Let’s use the same example of factoring a $100,000 invoice that’s due in 60 days. With tiered factoring the factor charges you different interest rates for different periods of time the invoice is outstanding. So say the factoring company charges 2.75% for 30 days and 5.5% for 60 days. Within a few days of factoring the invoice, $94,500 hits your account. If the invoice had been due in 30 days, the factor would’ve only withheld $2,750, instead of $5,500.

Prime plus margin rate fee example

Taking once again the example where you factor a $100,000 invoice that’s due in 60 days. In this scenario, the factoring company charges 5.5% for 60 days, plus the prime rate that day of 3 percent that applies to your entire invoice total (not just the advance rate). Your rate comes out to 8.5%. This means you end up paying $8,500 for a total advance of $91,500.

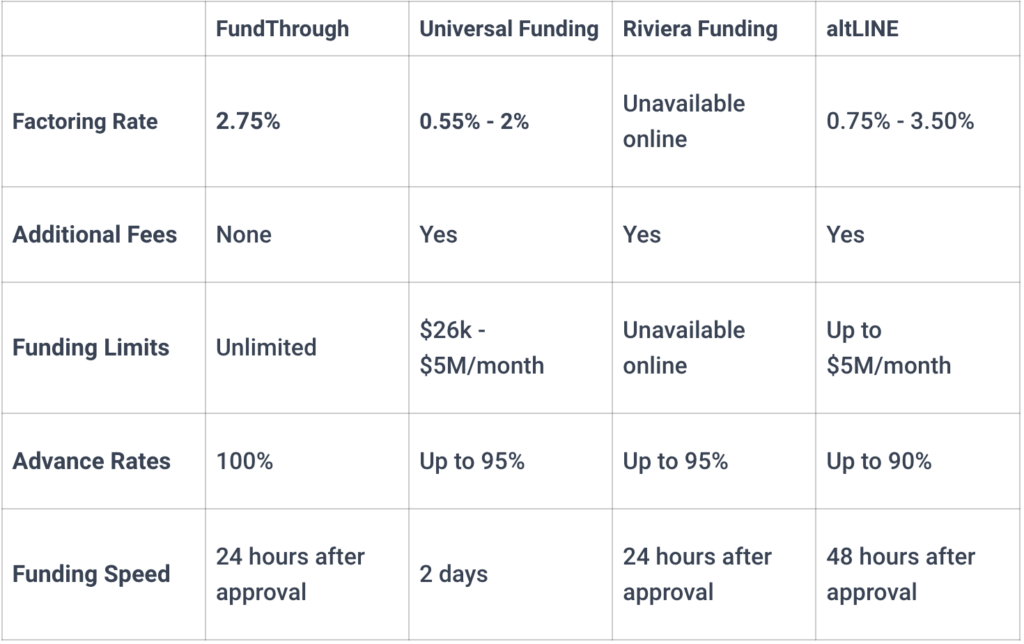

Factoring Rate Comparison

As you might expect, different companies offer different factoring rates. It can be challenging keeping everything sorted when comparing factoring fees. We’ve gone ahead and done the work for you to compare FundThrough’s invoice factoring rates, along with a few other important data points, with some other factoring companies, to hopefully make the process as simple as possible.

Invoice Factoring vs Banks: The True Costs

When CEOs and finance pros compare the price of factoring with their bank, the traditional route often appears to be a lot less expensive. However, we always suggest taking into account the overall cost rather than just the rate to make a fully informed decision.

If you pass on a big contract which could grow your business, is the bank truly saving you money? The value of a strong banking relationship is clear. However, if funding limits are also limiting growth, it may be time to explore creative funding methods like factoring. Businesses can maintain their valuable bank partnerships while simultaneously improving their cash flow (and avoiding more debt) simply by having their invoices paid quicker.

Offset factoring costs with your team structure

One creative way to offset factoring costs is by building factoring into your business so that you can structure your finance team around it. The account manager at your factoring company should keep you updated about the status of your A/R and help you manage it, eliminating the need for an in house AR specialist. (A factoring partner also brings added value through customer credit checks and proactively ensuring you’re well-capitalized.) Our clients regularly tell us that their account manager is a part of their team for those reasons.

Making Sense of Your Total Invoice Factoring Costs: Beyond the Rates

Understanding the difference between invoice factoring costs and rates is key to avoiding unexpected expenses. The factoring rate is just the percentage kept by the company for their services, but the real cost includes this rate plus any other fees, along with costs to factor more than you need to if you get locked into a contract that obligates you to fund invoices.

When looking at different companies, always ask for the full cost, not just the rate, and make sure they explain everything upfront. The cheapest rate might end up more expensive with all the extra fees and funding requirements.

FundThrough is all about being clear with costs from the start, with no hidden fees, and we even advance the whole invoice amount, not just 80%. We make sure you know exactly what you’re paying for, so there are no surprises later.

Invoice Factoring Rates FAQs

Your questions answered.

What are invoice factoring rates?

Invoice factoring rates range from 1-5% per month. They can vary based on several factors, including the volume and size of your invoices, industry risk, net terms, creditworthiness of your customers, and the type of rate (daily or transaction).

How can I find the best invoice factoring rate for my business?

Finding the best invoice factoring rate starts with choosing a creditworthy customer whose invoices have short net terms. From there, you’ll need to compare pricing–but the cheapest rate is not always the least expensive option. Many factoring companies charge a variety of fees on top of the transaction rate. Asking any company you’re considering about their fees will show you the overall cost.

What is a good rate for factoring?

A good rate for factoring is between 1 percent and 6 percent per 30 day net terms. Be mindful of additional fees to accurately compare pricing and ensure you get a good deal – not just a good factoring rate.

Is invoice factoring risky?

The short answer is that if your customers are creditworthy and pay their invoices reliably, any risk involved with invoice factoring is very low. If you’re factoring with recourse, you’re still on the hook for an unpaid invoice that you’ve advanced. However, most factoring companies will work with you to come to a fair solution. Still wondering if invoice factoring is risky for you? Read more here.

Do banks factor invoices?

No, banks don’t factor invoices. Banks are in the business of lending money. Banks do, however, offer different types of financing that can be complementary to factoring (if you can qualify and have time to go through the process).

Is invoice factoring considered a loan?

No! Invoice factoring is not considered a loan. That’s one nice thing about factoring: it’s not debt. You’re simply getting an advance on work you’ve already done. You don’t have to pay your advance back because your customer just pays their invoice to the factoring company. Once that happens, there’s no further commitment.

What Is Invoice Factoring?

If you’re asking yourself, what is invoice factoring?, know that it’s a form of financing where a business owner sells outstanding invoices to a factoring company for fast access to funds. The business owner receives cash for the invoice amount, usually less any fees, ahead of the payment terms. The business owner’s customer, who is responsible for paying the invoice, instead pays the invoice amount to the factoring company according to the original payment terms.

Invoice factoring also goes by the terms accounts receivable factoring or receivable financing.

Why Factor Invoices?

B2B businesses use invoice factoring for different reasons. Your company should consider making use of an invoice factoring solution if:

- Banks have turned you down for a business loan or line of credit, or you don’t want to be tied up in traditional bank loans or lines of credit.

- You need a quick boost of cash flow – in a few business days, rather than a few months.

- If you need reliable access to cash flow for paying daily expenses and/or fueling business growth.

- You’re a startup company without much credit history yet. In many cases, invoice factoring doesn’t require a credit check or high credit score because it relies on the credit rating of your customers. Even businesses with bad credit can still often qualify for invoice factoring.

- You have slow-paying customers. Many customers insist on 30, 60, and even 90 day net terms, which means you’re without payment for months, for work you’ve already completed.

- You want more time to focus on your business instead of chasing down late payments and managing your A/R.